Sky Protocol - $SKY

The Cheapest Cash-Flowing Asset in Crypto Right Now?

Disclosure: Not financial advice. Do your own research.

Setting the Scene

As novel as crypto tries to be, many aspects of traditional finance still apply.

Valuation. Cash flow. Competitive moats. Even the humble price-to-earnings ratio, concepts in the world of “number go up” speculation, are starting to carry weight. The irony is that crypto’s original ethos was to escape the inefficiencies of traditional finance. But the longer the industry survives, the more it starts to rhyme.

This wasn’t always the case.

For most of crypto’s short history, there were no stable, revenue-generating protocols. The market was dominated by narratives. “The future of money,” “smart contract platforms,” “Web3”, all chased adoption curves that hadn’t yet materialized. It wasn’t until “defi summer” of 2020 that things began to change. That brief period created a Cambrian explosion of decentralized finance - yield farming, automated market makers, decentralized exchanges, lending protocols. Suddenly, the idea that crypto could generate real income wasn’t a fantasy.

Then, everything came crashing down. After 2020, a brutal crypto winter set in. The terror of Gary Gensler’s reign pushed crypto offshores and outside the U.S. And don’t bother disputing this; I worked for a crypto company that was forced to relocate to Mexico City to avoid legal repercussions. The result was an exodus of talent and capital. From 2022 through 2024, the industry went dark. No bull market cycles. No token launches. No VC mania.

And yet, in all the silence, something important happened. Many builders stayed. Teams that survived the bloodletting spent those years refining “tokenomics”, improving protocol security, and figuring out how to generate sustainable yield. The result was a new generation of protocols that actually look, and behave, like financial businesses. They produce revenue, distribute profits, and compete on efficiency.

Now, in 2025, with a more pro-crypto administration in office and the regulatory fog lifting (especially thanks to the GENIUS act), investors are starting to pay attention again. But this time it’s no longer about revolution; the story of crypto shifted. It’s about convergence.

But in all the rediscovered hype, from memecoins - including the official Trump coin - to digital asset treasuries (DATs) and stablecoins, core defi protocols that are now actually generating strong net income are being ignored. Fintechs like Robinhood and Coinbase are stealing the show, focusing on tokenization and stablecoins.

Parallels to Traditional Finance

In traditional finance, banks form the backbone of the system. They take deposits, lend money, and profit from the spread, the difference between what they pay depositors and what they earn from loans. The largest U.S. banks, JPMorgan Chase, Bank of America, Wells Fargo, collectively hold over $5 trillion in deposits and generate tens of billions in net income annually.

At current valuations, these banks typically trade at around 1.5–2.0 time book value, and roughly 10-12 times earnings. For all the complexity of modern finance, their model is simple: borrow at 1%, lend at 5%, keep the difference, and don’t blow up. Investors value them for their stability, predictable cash flows, and scale.

In crypto, there are no banks. There are no tellers, no branch offices, and no centralized ledger managed by a corporate entity. Instead, you are your own bank. Every computer in the network keeps a synchronized record of ownership, ensuring that no single party can alter balances or rewrite history. If a participant tries to cheat, they’re punished, “slashed”, by the network’s consensus mechanism.

But crypto didn’t stop at storing value. It recreated banking itself. This time, in code.

In place of traditional banks, crypto has “money markets”: decentralized lending platforms that allow users to deposit, borrow, and earn yield, all governed by transparent smart contracts. Think of them as algorithmic banks that live “on-chain”.

Sky Protocol

One of the most successful money markets is Sky Protocol, originally known as MakerDAO. Maker pioneered decentralized stablecoins and lending long before “DeFi” became a buzzword. It acts as the crypto equivalent of a central bank and a money market rolled into one. Users deposit crypto collateral, mint stablecoins, and pay interest. That’s income that accrues to holders of the SKY governance token.

But let’s wind back the clock.

MakerDAO didn’t just change its name. It reinvented itself. The transition to Sky Protocol marked the culmination of nearly a decade of evolution. Maker had grown from a niche crypto experiment into a multi-billion-dollar on-chain financial system. Its stablecoin, DAI, became the backbone of DeFi, but its governance model was showing cracks: too many decisions bottlenecked through token holders, too little flexibility to adapt, and too much dependence on external collateral like USDC.

The rebrand to Sky Protocol was more than cosmetic. It’s an attempt to evolve from a decentralized stablecoin project into a full-fledged crypto central bank. Sky refocused on scalability, sustainable yield, and modular governance. It built new layers (like Spark and Endgame) to separate risk management from day-to-day operations, creating a system that could actually scale without collapsing under the weight of committee politics. In essence, Sky Protocol is MakerDAO’s grown-up form - cleaner, more autonomous, and more financially coherent.

The Architects

The story of MakerDAO, and by extension Sky, starts with Rune Christensen, a Danish entrepreneur who founded Maker in 2015. Rune’s vision was audacious for its time: a decentralized credit system that could issue a stable currency without banks or governments. Under his leadership, MakerDAO survived multiple crises - the 2018 crash, the 2020 “Black Thursday” liquidation event, and the multi-year DeFi bear market. All the while iterating on one of the most complex token economies in crypto.

By 2024, Rune and the core contributors realized Maker’s original architecture had reached its limits. Governance fatigue, reliance on real-world assets, and creeping centralization made the system fragile. The team, a mix of early Maker veterans and new technical leads, decided it was time for a reboot. Thus Sky Protocol was born. Same DNA, new body. Rune remains the ideological anchor, but Sky now operates more like a federation of autonomous sub-DAOs, each responsible for a piece of the financial stack.

Modern Valuation

Let’s start with how Sky Protocol is behaving more like a bank than a memecoin. Much like institutions such as JPMorgan Chase or Wells Fargo earn a spread on deposits and loans, Sky earns via fees and revenue on its on-chain “balance sheet.” Except, as we mentioned, there is no CEO, no board, and no FDIC insurance. Its operations are transparent, rules enforced by smart contracts, and revenues distributed to token holders.

According to data from DeFi Llama, Sky has annualized fees of approximately $416.2 million and revenue of about $193.7 million. Of that revenue, annualized earnings are around $184.1 million. The protocol’s market cap at the time was about $1.361 billion.

So let’s map this to traditional finance metrics:

Earnings (aka net income): ~$184 m

Market cap: ~$1,361 m ⇒ implies a P/E of ~7.4x

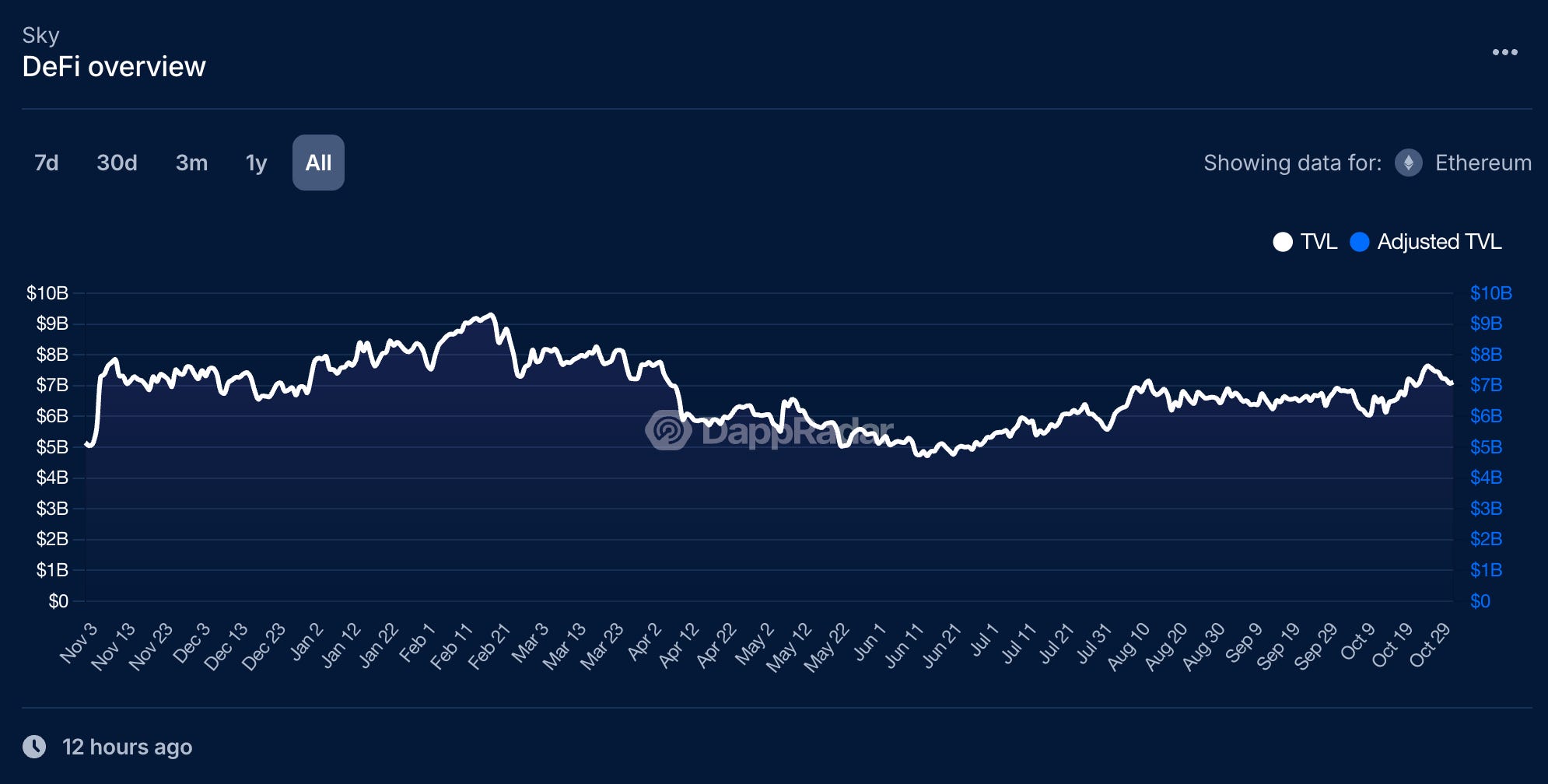

Fees vs. TVL: With TVL at roughly $7.435 b (per DeFiLlama), the annualized fee yield is ~5.6%.

Revenue yield: ~$193.7 m over $7,435 m is roughly 2.6%

In banking terms: if Sky were a bank, you’d say it earns about 2.6% of the assets as revenue per year, and the market is pricing the equity (token) at ~7.4x earnings. That’s a bargain compared to many traditional banks, where earnings multiples might run 10-12x or more depending on growth.

Now, of course the caveats: banking earnings are more stable historically; DeFi protocols carry protocol risk, regulatory risk, and token dilution risk. DeFi is also less sticky. As new protocols and tokens are launched, higher yield moves elsewhere, attracting liquidity. Sky needs to continue to execute well to steadily grow these deposits. Though, looking at the chart below, TVL has been impressively consistent.

The point is this. Protocols like Sky are beginning to reach the scale and financial maturity where traditional valuation metrics - P/E ratios, book value, return on equity - actually start to make sense. For the first time we can compare a decentralized protocol to a bank and not sound insane. As more protocols stabilize and mature, equity investors will begin to look at digital assets similarly to equities.

Treasury Adjustments

A protocol’s treasury is a real on-balance-sheet asset. One conservative way to think about it: subtract liquid treasury value from market cap to get an “operating” market cap (i.e., market cap net of reserve assets). TokenTerminal lists the treasury at $354 million.

Net market cap = 1,300,981,846 − 353,500,000 = $947,481,846.

While the Treasury is starting to provide a “book value”, the token isn’t doing so well. It’s down nearly 50% since August highs.

Now let’s recompute P/E (using the net market cap): 947,481,846 / 143,040,000 ≈ 6.62. So when you account for the treasury, the token is effectively trading at ~6.6x holders cashflow, materially cheaper than the headline ~9.1 multiple.

Some other interesting ratios worth noting:

Treasury as % of market cap: 353,500,000 / 1,300,981,846 ≈ 27.2% of market cap held in the treasury right now. That’s a big cushion.

Fee yield on TVL (fees / TVL): using DeFiLlama fees ≈ $424.6M and DeFiLlama TVL ≈ $7.075B, fee yield ≈ 424.6 / 7,075 ≈ 6.0% annualized on locked assets. (this is a rough protocol-level APR).

Buybacks

Now here’s where it gets interesting.

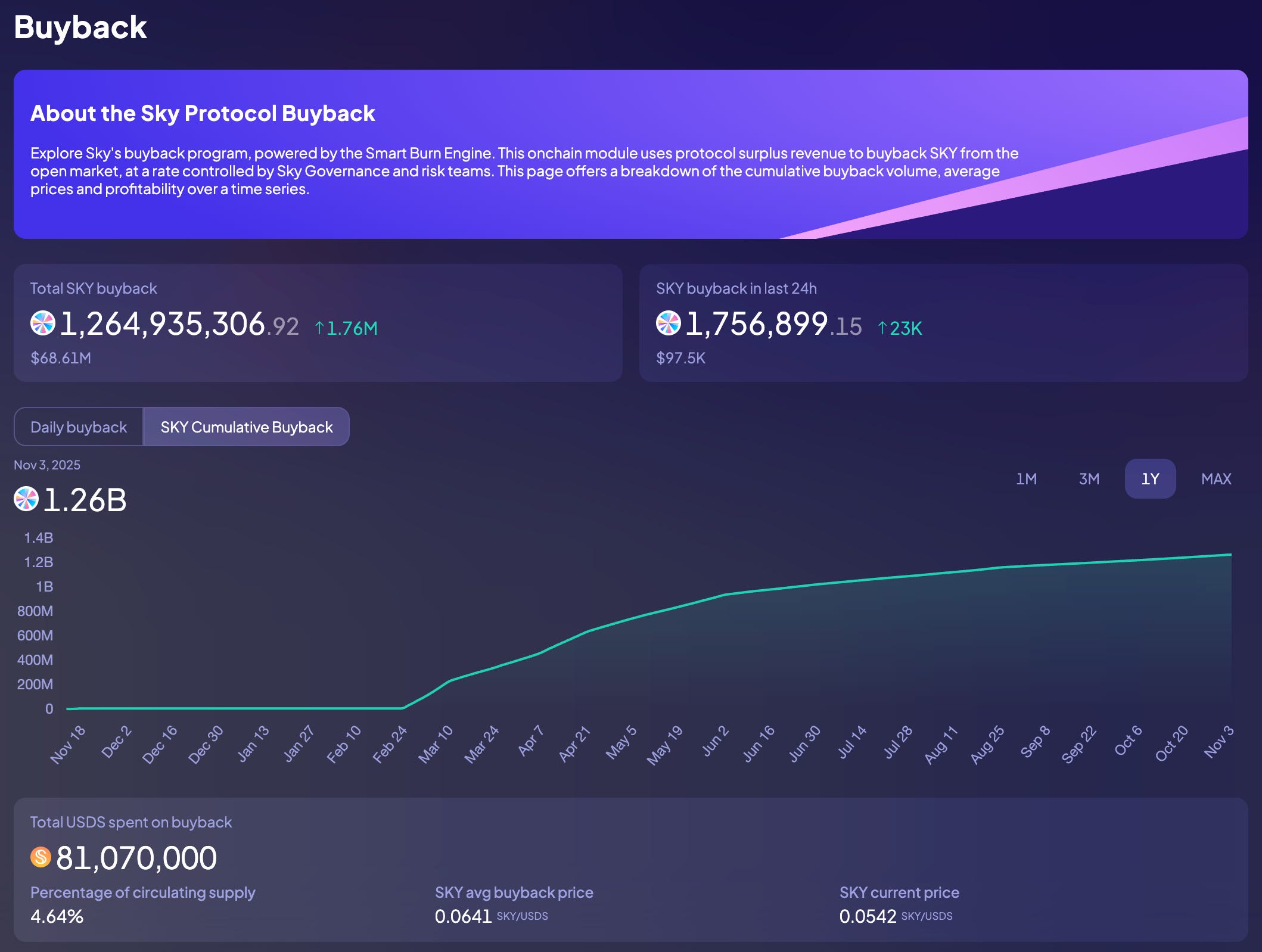

Buybacks are Sky’s quiet engine of value creation. Instead of paying dividends, the protocol uses revenue from its stablecoin and lending operations to repurchase SKY tokens on the open market, permanently removing them from circulation. Recent governance updates increased daily buybacks to roughly $300,000 in USDS, with over 1 billion SKY already retired to date. Each buyback reduces supply while directing protocol cash flows back to holders - effectively the DeFi version of a stock repurchase program. Sky Protocol even tracks buybacks through their own dashboard.

For investors, the math is clear. If earnings stay constant while circulating supply falls, each remaining token claims a larger share of future cash flows. Combine that with Sky’s growing treasury and stable on-chain revenues, and buybacks become a built-in yield mechanism, a steady, automated return of capital to long-term holders. In traditional finance terms, it’s like owning equity in a bank that uses its profits to buy back shares every single day.

Conclusion

If you factor in Sky’s ~$350 million treasury, its effective market cap falls to roughly $950 million against about $184 million in annualized earnings, an implied P/E of just 6.5x. If investors valued it like a traditional bank at 10x earnings, Sky’s core operations alone would be worth $1.84 billion, and adding back the treasury brings total value near $2.2 billion. That’s nearly a 70% upside from today’s levels. Even at a conservative 8x multiple, Sky would still clear $1.8 billion including treasury, while modest earnings growth and a 12x multiple would push valuation toward $2.8 billion.

Ontop of this, Sky’s buybacks add a powerful second layer of upside on top of its valuation gap. At the current $300,000 per day buyback pace, the protocol repurchases about 6% of total supply annually. In traditional equity terms, that’s a 6% annual “buyback yield”, funded directly from protocol cash flows. If the market re-rates Sky toward its fair value and buybacks continue for a full year, investors effectively capture both the revaluation and the incremental value per token from reduced supply. In simple compounding terms, a 70% price re-rate combined with 6% annual supply reduction yields roughly 78% total upside over the next year, assuming fundamentals hold steady. Extending the time horizon out further significantly further steepens this upside.

On the flip side: if protocol growth stalls, or regulatory headwinds bite, the multiple could compress and market cap shrink. So the valuation hinges on two levers: earnings growth and multiple expansion (or contraction).

In short, Sky generates real income, has meaningful assets under management, and the token is closer to equity than a memecoin. If you adopt that mindset, then modeling SKY using traditional finance tools isn’t crazy, it might be the right method.

Let us know what you think in the comments, or message us in our chat.