Grab

The Superapp of South East Asia

Disclosure: Not financial advice. Do your own research.

Introduction

Grab Holdings is an inexpensive, fast growing superapp turning GAAP profitable. The company has extremely fast growing free cash flows, $7 billion in cash, and is poised to gain significant operating leverage. Grab is such a strong business that they even drove Uber out of business in Southeast Asia, convincing Uber to hold a stake in GRAB 0.00%↑ till this day. Grab operates in South East Asia, across eight countries, but, the stock is not an ADR; it’s a direct listing on the NASDAQ.

This is our thesis.

Background

In the bustling halls of Harvard Business School in 2011, Anthony Tan, a Malaysian entrepreneur hailing from a prominent automotive family, conceived an idea that would revolutionize mobility in Southeast Asia. Frustrated by the inefficiencies and safety concerns of traditional taxi services back home (issues he discussed with classmate and future co-founder Tan Hooi Ling) the duo entered a business plan competition with a concept for a ride-hailing app. Drawing from personal experiences, including friends’ harrowing encounters with unreliable cabs, they aimed to create a safer, more efficient alternative. This vision materialized in 2012 with the launch of MyTeksi in Kuala Lumpur, Malaysia. The two started small with just 20 taxi drivers and a modest office in a garage. But the app quickly gained traction, rebranding to GrabTaxi in 2013 and expanding beyond rides to include motorbikes and private cars, tapping into the region’s diverse transportation needs.

As Grab evolved, it aggressively expanded across Southeast Asia, entering markets like Singapore, Indonesia, and Vietnam by 2014, fueled by substantial venture funding and a focus on localization. The team masterfully adapted services to local languages, payment methods, and cultural preferences. Then, in 2018 a pivotal moment arrived. In a landmark deal, Grab acquired Uber’s Southeast Asian operations, solidifying its dominance in ride-hailing while integrating food delivery through GrabFood and financial services via GrabPay. This transformation turned Grab into a “super app,” offering everything from deliveries and digital wallets to insurance and lending, serving over 200 million users. By 2021, the company went public on NASDAQ through a SPAC merger, valuing it at around $40 billion at its peak. Less than two years later, the stock collapsed 80%. For multiple years, GRAB 0.00%↑ remained in the gutter, consolidating between $2-4 per share, until now.

All the meanwhile, the Grab business grew stronger. As of today, Grab stands as Southeast Asia’s leading super app, achieving GAAP profitability and pushing the boundaries of innovation through EV integrations and autonomous ride-share pilot programs. Under Anthony Tan’s leadership, the company has weathered economic challenges, including the COVID-19 pandemic, by pivoting to essential services like grocery delivery and financial inclusion for the unbanked. With operations in eight countries and a valuation hovering around $15-20 billion, Grab’s journey from a Harvard brainstorm to a regional powerhouse is nothing short of legendary.

Anthony Tan

For Anthony Tan, founder and current CEO of Grab, that journey came at a cost. He grew up in one of Malaysia’s richest families as the youngest son of Tan Heng Chew, who leads the massive automotive company Tan Chong Motor. Tan could have slipped into a ready-made role of wealth and power. But he chased a bolder dream to reshape transportation across Southeast Asia. When he quit the family business to start Grab, his father cut him off, calling his startup idea foolish with the words, “Your head is in the clouds.” This break hurt deeply. It stripped away his safety net and family support, pushing him to risk it all on a concept sparked during his time at Harvard Business School.

Still, Tan’s grit powered him forward. Driven by a fierce hunger to make a difference, he threw himself fully into Grab. He began in a simple garage office, fighting through early setbacks, investor doubts, and tough regulations in the region. He went all in, giving up not just family ties but also the easy life he knew. This can’t be emphasized enough. He’s been quoted as saying he worked 16, 18, 20 hours per day, Monday to Sunday.

You can sleep all you want when you’re dead.

- Anthony Tan, lessons from his grandfather.

That passion turned a basic taxi app into a giant super app that now helps millions every day. It reached profitability even through hard times and stiff rivals. Tan’s path shows the tough side of starting something big. Real change often means betting more than money. It demands your whole heart.

Anthony Tan sets the bar for the ideal founder-owner-operator. Although he owns a relatively small 3.3% stake in Grab, his devotion is unrelenting. He’s the type of individual that lends conviction; he’s the difference maker. Because when all else fails - when growth subsides, regulation ensues, competition appears - your investment in Grab lies with Anthony Tan. And that’s a bet that’s worthwhile to make.

Consolidation

Grab’s story isn’t all sunshine and rainbows.

South East Asia, like all places is a fiercely competitive market. When Grab launched as MyTeksi in Malaysia in 2012, it quickly clashed with global giant Uber, which had entered the region around the same time. The rivalry intensified as both companies vied for dominance in ride-hailing, with Grab differentiating itself through cash payments and localized features tailored to Southeast Asia’s diverse needs. By 2018, after years of heavy subsidies and market battles that burned through billions in investor cash, Grab struck a deal to acquire Uber’s Southeast Asian operations, including Uber Eats. In exchange, Uber received a 27.5% stake in Grab, effectively exiting the region and handing Grab over 95% of the ride-hailing market share at the time. This acquisition not only eliminated a major competitor but also accelerated Grab’s pivot to a super app, integrating food delivery and expanding its user base to millions across eight countries. Today, Uber still holds a roughly 13-14% stake in Grab.

Aside from Uber, Grab has absorbed, or outmaneuvered, other players through strategic acquisitions and aggressive expansion. In 2017, it acquired Indonesian fintech startup Kudo to bolster its digital payments arm, GrabPay, targeting the unbanked population and enhancing its ecosystem. More recently, in 2022, Grab bought a majority stake in Malaysian supermarket chain Jaya Grocer to strengthen its grocery delivery offerings amid rising e-commerce demand. These moves have helped Grab edge out competitors like Foodpanda and Deliveroo in food delivery, where it now commands about 50-55% market share regionally, while pressuring smaller local apps to consolidate or fade. In ride-hailing, Grab’s duopoly with Gojek in Indonesia (where each holds roughly 50%) contrasts with its near-monopoly elsewhere, such as 97% in Malaysia and 91% in the Philippines as of 2025. Later on in this writeup, we’ll review Grab’s position in each of the eight countries Grab competes in.

Today, Grab’s dominance is evident in its 72% combined market share in mobility and delivery across Southeast Asia, achieved through relentless innovation and outlasting rivals in a subsidy-driven war of attrition. While it hasn’t directly driven many others out, preferring acquisitions to consolidate power, the company’s growth has marginalized players like ShopeeFood in certain markets and fueled discussions of potential mergers, such as with Gojek’s parent GoTo, to further solidify its position. This history underscores Grab’s transformation from a scrappy startup to a regional powerhouse, often at the expense of competitors unable to match its scale and adaptability.

Even more crucial than outmaneuvering competitors is achieving true profitability. Grab’s path to GAAP profitability was a grueling one, marked by years of intense battles that devoured massive amounts of capital, especially in its high-stakes showdown with Uber. Today, few rivals can boast meaningful market share, let alone positive cash generation. Take GoTo, the parent of Gojek: it has hemorrhaged cash throughout its existence, with no clear path to profitability on the horizon. This disparity gives Grab powerful leverage for potential mergers and acquisitions, which seem increasingly likely. In short, Grab stands in a commanding position of strength.

Regional Tailwinds

Southeast Asia stands as one of the world’s last frontiers where a massive wave of people is rapidly coming online. It will fuel unprecedented digital and economic momentum. While much of the globe already boasts high internet penetration, the region, home to about 700 million people in 2025, is projected to grow to over 741 million by 2035, driven by population momentum even as fertility rates hover around the replacement level of 2.1 births per woman. Currently, nearly 80% of the population, or over 550 million users, is connected, a figure that has tripled in the past decade thanks to affordable smartphones and expanding infrastructure. Over the next 10 years, as penetration climbs toward 90% or higher amid this demographic swell, the number of internet users could surge to around 670 million, unlocking vast opportunities in e-commerce, fintech, and digital services that supercharge consumer spending and innovation.

We think this demographic boom, paired with a youthful population and rising connectivity, acts as a powerful tailwind propelling Southeast Asia’s GDP growth to outpace many global peers. The region is forecast to expand at 4.3% annually through 2026. Some longer-term projections suggest sustained growth into 2035 as urbanization and middle-class expansion drive demand. Unlike stagnating economies elsewhere, SEA’s blend of population growth and digital adoption is expected to boost per capita income and attract foreign investment. This could potentially lift the combined GDP from around $3.7 trillion today to over $6 trillion by 2035. As more people come online and enter the workforce, grab is positioned as their digital onramp.

Competition

It’s no secret that Grab faces competition. The rideshare and delivery markets are complex across the various South East Asian companies, each with their own quirks and challenges. Although Grab has a dominant position in many of the eight countries it operates in, the company faces competition from both local and regional players in ride-hailing, food delivery, and other services. Let’s break down the competitive landscape by country, focusing on key competitors. Note that competition varies by service type. Some competitors like Gojek also offers a compelling super-app similar to Grab.

Cambodia: Competitors are TADA, FastGo. Grab dominates in ride hailing (estimated at 80%) and delivery at roughly 50%.

Indonesia: Many competitors - Gojek, Be, Xanh SM, InDrive, Maxim, Foodpanda, ShopeeFood. Grab dominates at roughly 50% marketshare for both ride hailing and food delivery.

Malaysia: Competitors are Foodpanda, InDrive, Maxim. Grab makes up 97% for ride hailing and 50% for food delivery.

Myanmar: No notable competitors. Grab services the vast majority of both.

Philippines: Competition is Foodpanda, JoyRide, inDrive, Maxim, Gojek, HonestBee. Grab accounts for 90% of ride hailing, and about 50% of food delivery.

Singapore: Competitors are Gojek, Foodpanda, Deliveroo, CDG Taxi (ComfortDelGro), TADA, Ryde, Maxim, Be. Grab is at 83% of ride hailing and 65% of food delivery.

Thailand: Competition is Gojek, ShopeeFood, Be, InDrive, Maxim, TADA. Grab handles 85% of ride hailing and around 50% of food delivery.

Vietnam: Multiple competitors being Gojek, ShopeeFood, Xanh SM, Be, InDrive, Maxim, TADA. Grab is only 36% of ride hailing and 47% of food delivery.

Grab X

GrabX marked a pivotal inflection point in Grab’s history, signaling the company’s bold step into a new era of innovation and transparency. On April 8, 2025, Grab hosted its inaugural GrabX product showcase in Singapore, unveiling a suite of AI-powered features and services under the theme “For Every You.” This event, reminiscent of Robinhood’s high-profile product announcements that propelled it into the spotlight, isn’t just about revealing what’s next. It serves as a reflexive mechanism, compelling Grab’s teams to accelerate development and deliver tangible results. As CEO Anthony Tan took the stage, the live streamed presentation acted as a forcing function, setting a clear deadline for shipping products and creating internal alignment around ambitious goals. In a region where local tech firms rarely stage such events, GrabX broke the mold, demonstrating confidence in its product pipeline and a commitment to engaging users and investors directly.

What’s really special about GrabX is its role as a rallying point, turning visibility into velocity. By publicly committing to launches like GrabFood for One (curated affordable solo meals), Grab for Family and Teens (family-linked accounts with safety features), Shared Saver (group ride-sharing for cost savings), Advance Booking for airport pickups, Dine-Out Discovery powered by GrabMaps, and the Grab Travel Pass, Grab is establishing a cadence for ongoing innovation. These additions, built on Grab’s massive network of 45 million monthly users, aim to deepen engagement and expand total addressable market (TAM) in food delivery, mobility, and beyond. Despite some production hiccups in the first event, the initiative underscores Grab’s hunger to turn up the heat, as it forces the company to iterate rapidly and outpace competitors. If Grab maintains this annual rhythm, introducing 4-5 meaningful products yearly, it will solidify its moat through enhanced platform stickiness and drive sustained topline growth. Not only that, it gets people excited about using Grab and its new features.

Financials

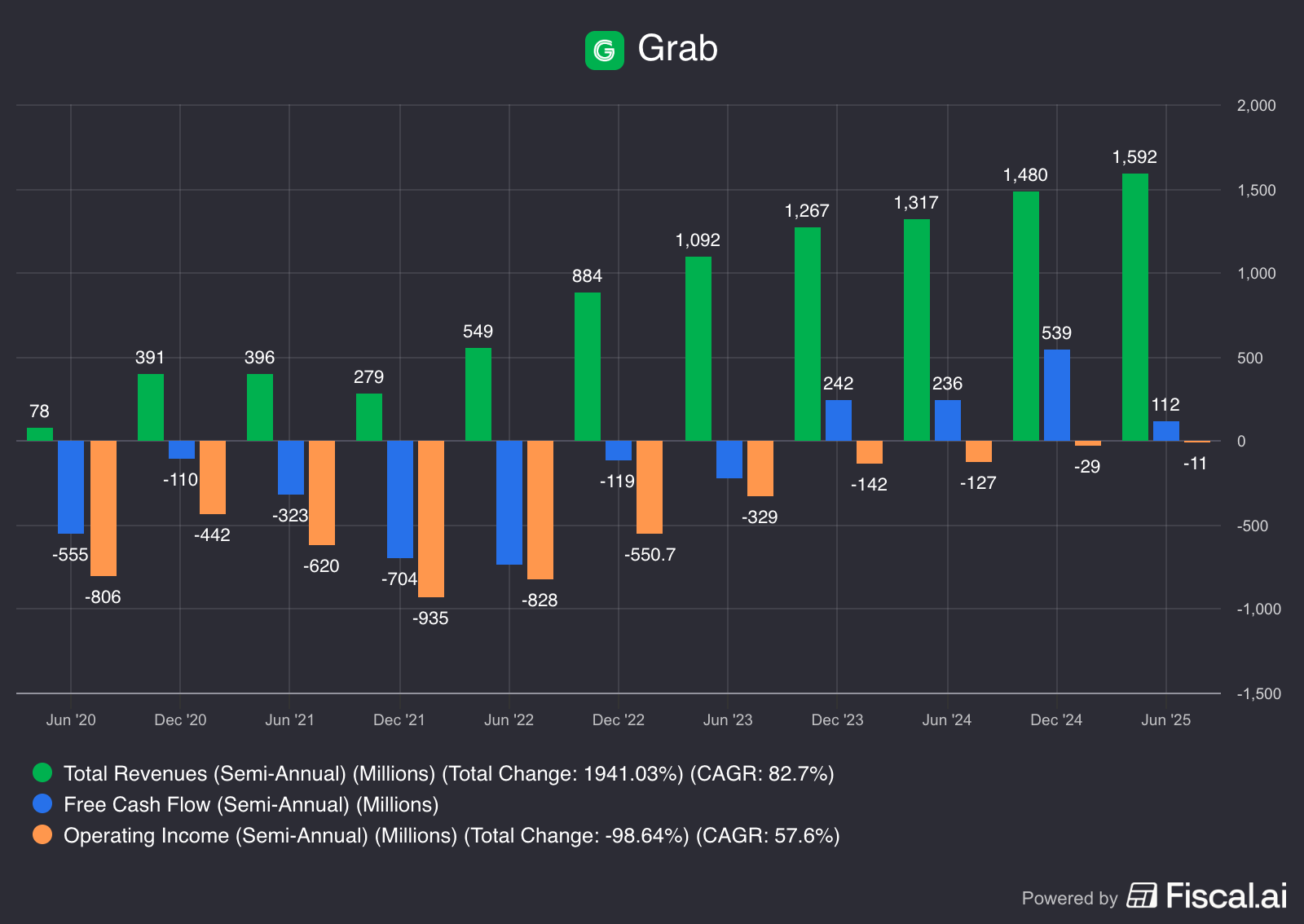

Below, we’ve compiled semi-annual financials for Grab with Fiscal.ai (great site by the way). Semi-annual view helps give historical data for the covid-era where Grab reached it’s lowest operating income.

Right now, Grab is only just starting to turn a GAAP profit. This is important. Even though Grab had significant cash reserves in the past (roughly $7 billion cash now), they were largely burning cash. Burning cash requires a different operating approach, where keeping cash on the sidelines is a necessity. Now is an inflection point. The business is self sustaining, there’s no need to hold $7 billion in cash on the balance sheet. It’s burning a hole in their pocket. We expect that they’re increasingly inclined to deploying it.

Financial Services

Mobility and delivery are wonderful businesses, and Grab is crushing it. But they’re linearly driving operating leverage. We think the bread and butter lies in other services on the Grab superapp. The value prop of Grab is: come for the rideshare and food deliver, stay for the rest of the product suite. Currently, two of these services are advertising and financial services. But we expect Grab to continue to ship net new products and services, in the near future.

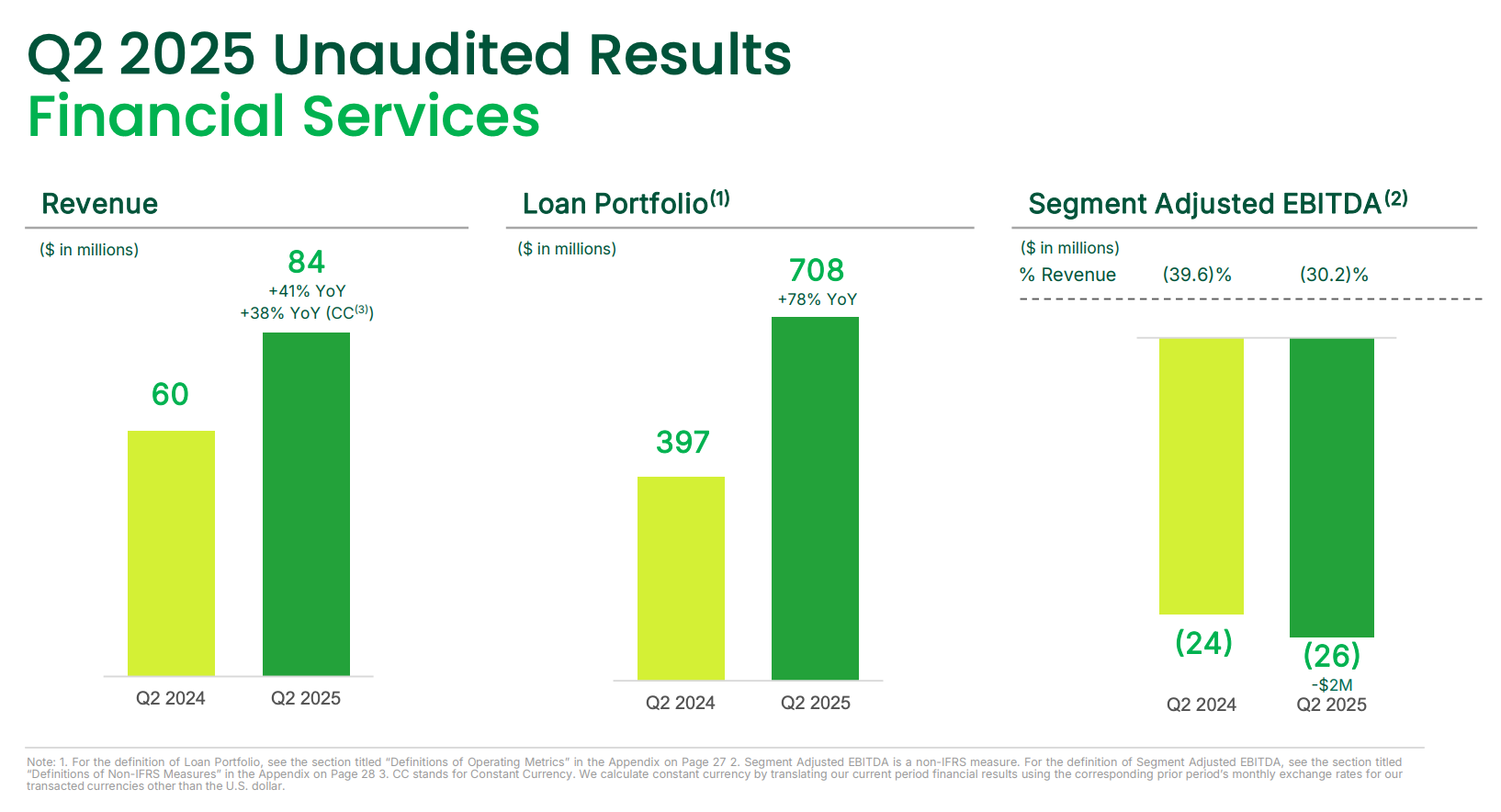

Focusing on financial services, Grab’s loan portfolio growth is accelerating. They anticipate a loan portfolio of over $1 billion by the end of 2025. That’s incredible. Financial services is currently growing at a clip of 40%, which is the fastest growing part of the business. By the end of 2026, the financial services business is expected to break even.

Look, financial services is an incredibly difficult and competitive business in-it-of-itself. But, we think Amits Deep Dives nails it in his Grab thesis.

While fintechs are an incredibly competitive business, the tailwind that Grab has is that almost half of the people in the SEA region are underbanked. This means if Grab can create brand awareness with all these users with ride hailing or deliveries and then continue to occupy their mindshare, eventually they can promote a banking product or payment product to them which would lead to more net deposits.

The key insight is that Grab already has a strong brand. That is a moat. It’s a sticky, consumer-focused app. Why would you bank with some random third party when Grab, a service you may use daily for rides or delivery, offers those same or better product offerings?

When you engage with Grab’s services, you’re sharing valuable data that helps the company build a detailed model of your interactions across its ecosystem. This insight becomes a powerful asset as you explore their banking products. It allows Grab to customize offerings precisely to your profile. From personalized loans to specialized financial tools, everything is tailored to align with your unique needs and behaviors.

On the merchant side of Grab’s business, the flywheel may spin even more tightly. Merchants rely heavily on Grab to connect them with customers and promote their listings effectively. To foster stronger partnerships, Grab provides essential services like advertising, loans, and its new AI assistant. Merchants who adopt these tools grow increasingly invested and dependent on the platform, which in turn enables Grab to pour more resources back into supporting them. This compounding dynamic not only deepens loyalty but also draws in new merchants eager to tap into the momentum.

What’s most exciting? We think banking is only a small part of the service suite that Grab has to offer in the future. Grab is extremely committed to solving real user problems. With over half of the Southeast Asia region being underbanked, Grab has a real opportunity to capture a significant portion of the financial services sector. As they scale up, we expect GRAB 0.00%↑ to be break-even on financial services in 2026.

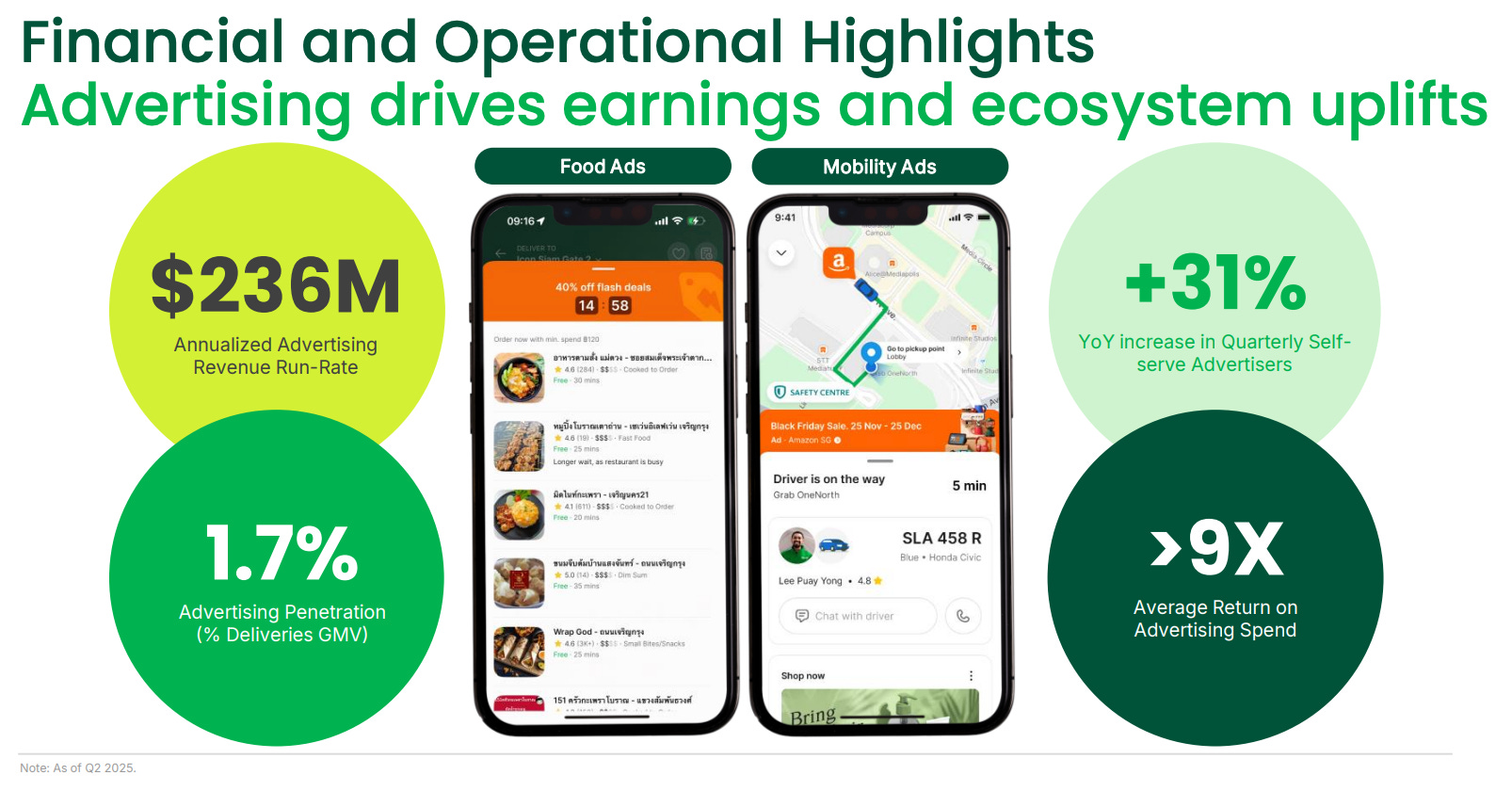

Advertising

Grab’s advertising segment, known as GrabAds, has emerged as a high-growth pillar within its superapp ecosystem, leveraging the platform’s vast user base and data insights to drive targeted promotions. As of Q1 2025, Grab boasted 191,000 active advertisers, representing just 3% of its 6 million merchants, with advertising revenue contributing 1.7% of deliveries gross merchandise value (GMV). That’s up from 1.3% the previous year. By Q2 2025, this segment achieved a 31% year-over-year growth, reaching an annualized run-rate of $236 million, fueled by self-serve tools that simplify ad creation and placement for small merchants. Advertisers are drawn to Grab due to its 46 million monthly transacting users and sophisticated targeting technology, which uses transaction data from rides, deliveries, and payments to deliver personalized ads, yielding an impressive 9x return on ad spend. This network effect amplifies as more users join, creating a larger audience pool that enhances ad effectiveness, while features like the AI Merchant Assistant further refine recommendations and boost merchant engagement.

The beauty of Grab’s advertising model lies in its potential for near-term profit flow-through to the bottom line, as ads operate with minimal incremental costs and high scalability. Unlike mobility or deliveries, where take rates hover around 15-25% but involve operational expenses like driver incentives, advertising boasts near-100% gross margins after platform fees, allowing revenue gains to directly bolster EBITDA without proportional cost increases. Management has signaled room to expand ad take rates beyond 1.7% - potentially to 2.2% or higher by 2026 - through better targeting tech and user growth. That could add $183 million in annual revenue per percentage point increase. This compounding dynamic, absent the need to raise core service fees, positions Grab for margin expansion on its path to sustained profitability. Analysts project ad revenue to double or more in the coming years as penetration among merchants rises from the current low base.

Outlook

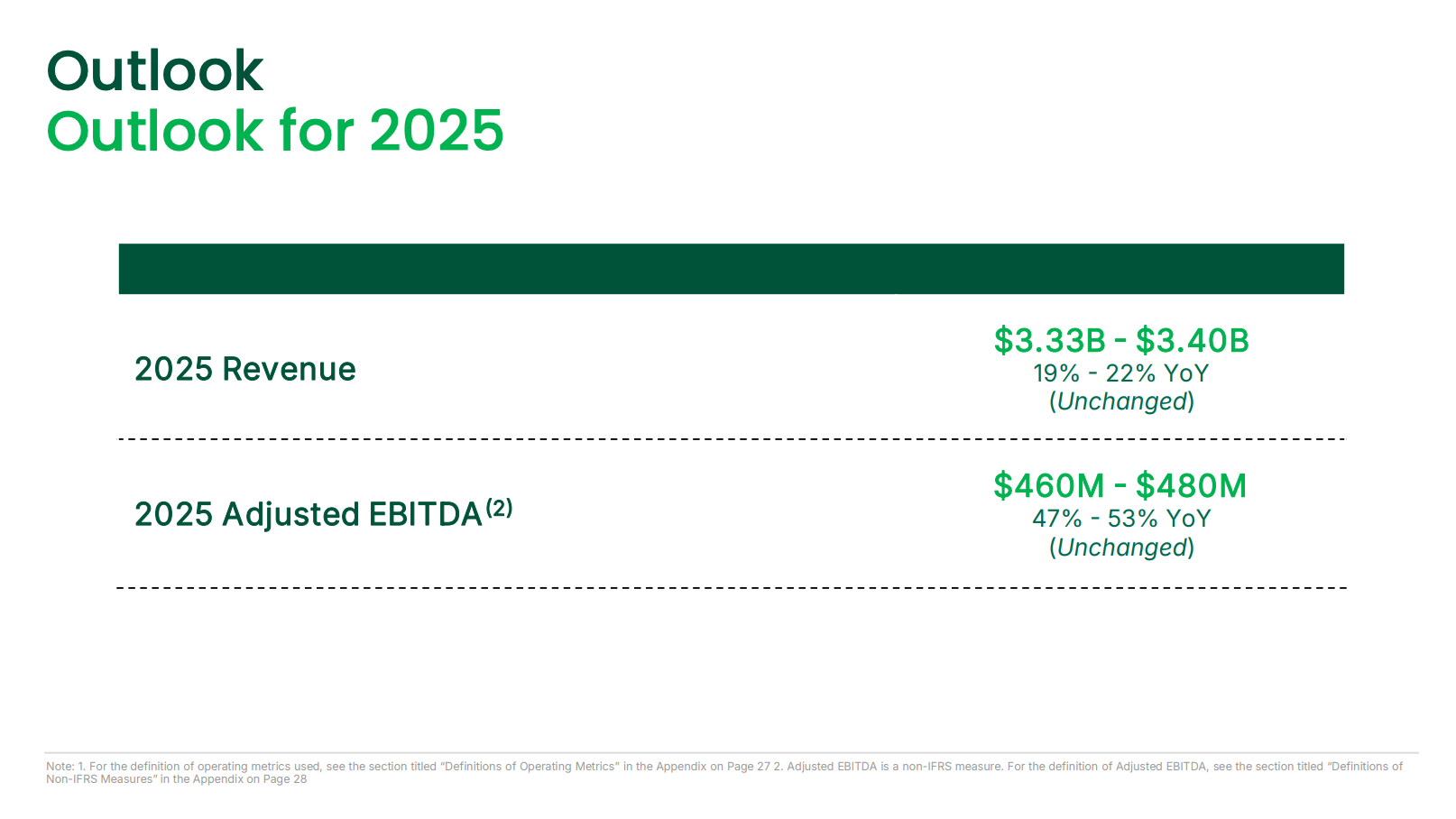

The guidance for EBITDA is incredible. In fiscal year 2024, Grab’s EBITDA was -9 million according to Fiscal.ai. A guidance of nearly $500 million is tremendous growth. If Grab is able to continue to grow the bottom line like this, the stock will get a re-rating, and soon.

Profitability aside, growth of 19-22% is impressive at scale. On the upper end of this guidance, Grab would be experiencing accelerated top-line growth, with the last two years of growth being 18.6% and 18.9% respectively.

Risks

There are a number of risks to the Grab thesis. It’s not perfect. Structural changes can happen, management can change, and external factors will come into play. Here, we’ll outline a pre-mortem of what could go wrong.

Margins remain low.

Our expectation is the classic operating leverage argument. As the top-line grows, operating expenses grow much slower or could decrease if management executes exceptionally well, resulting in margin expansion. Usually companies require debt to gain operating leverage, especially when they are young and don’t have large free cash flows. Grab has both: large, growing free cash flows paired with a very strong balance sheet with $7 billion in cash. There’s plenty of organic, non-debt fuel for Grab to achieve operating leverage.

FX Headwinds

There’s not much that can be done about this. If the US Dollar increases in strength, Grab’s FX adjusted return decreases. Where we expect this to be mitigated is through international expansion, and as such, diversification. Grab already operates in 8 countries as of late 2025. That number is only increasing. In fact, recently Grab made its first push out of South East Asia, bringing its mapping technology to Mongolia. In the future, Grab may expand its superapp offerings to more international markets including Mongolia.

Regulation

Grab has already driven a lot of competition away, paving the way for it to be in a monopolistic position. Although we expect the landscape to evolve similarly to the US where rideshare is a duopoly or oligopoly, Grab may experience regulatory pressure to avoid it from becoming a monopoly.

Operational Risk

Anthony Tan has repeatedly emphasized that the biggest risk for Grab is stagnation. He believes that Grab will only succeed if it continues to reinvent itself. We don’t think there’s much reason for this to change, and Grab X gives us an annual event to gauge progress.

Catalysts

It’d be remiss not to mention important catalysts that could invite a re-rating.

Acquisitions. Grab has a $7 billion cash pile. It’s not just sitting there for management’s joy. We think there’s a high chance Grab performs one or multiple acquisitions. In fact, there’s long been rumors that Grab would acquire Goto, a smaller Indonesian rival in the rideshare space. Although, both companies have repeatedly denied the gossip.

Grab X 2026. The inaugural Grab X 2025 took place on April 8th. A whole slew of new products and services were announced. There will likely be a number of new innovations released in April 2026 or whenever Grab X 2026 takes place.

Partnerships. Grab has already been engaged in several partnerships, with the most recent one being May Mobility. Along with Toyota and WeRide, Grab’s partnership with May Mobility expands its efforts to bring autonomous rides to the South East Asia region, on its platform. Future partnerships could act as a catalyst, especially for new digital offerings like integrated financial services.

Shareholder Returns. Deploying capital is difficult. Deploying it effectively even moreso. If Grab continues on its current trajectory, delivering strong profitability, it will only become more difficult to deploy its cash. In this case, we suspect Grab may begin share buybacks to effectively return excess capital to shareholders.

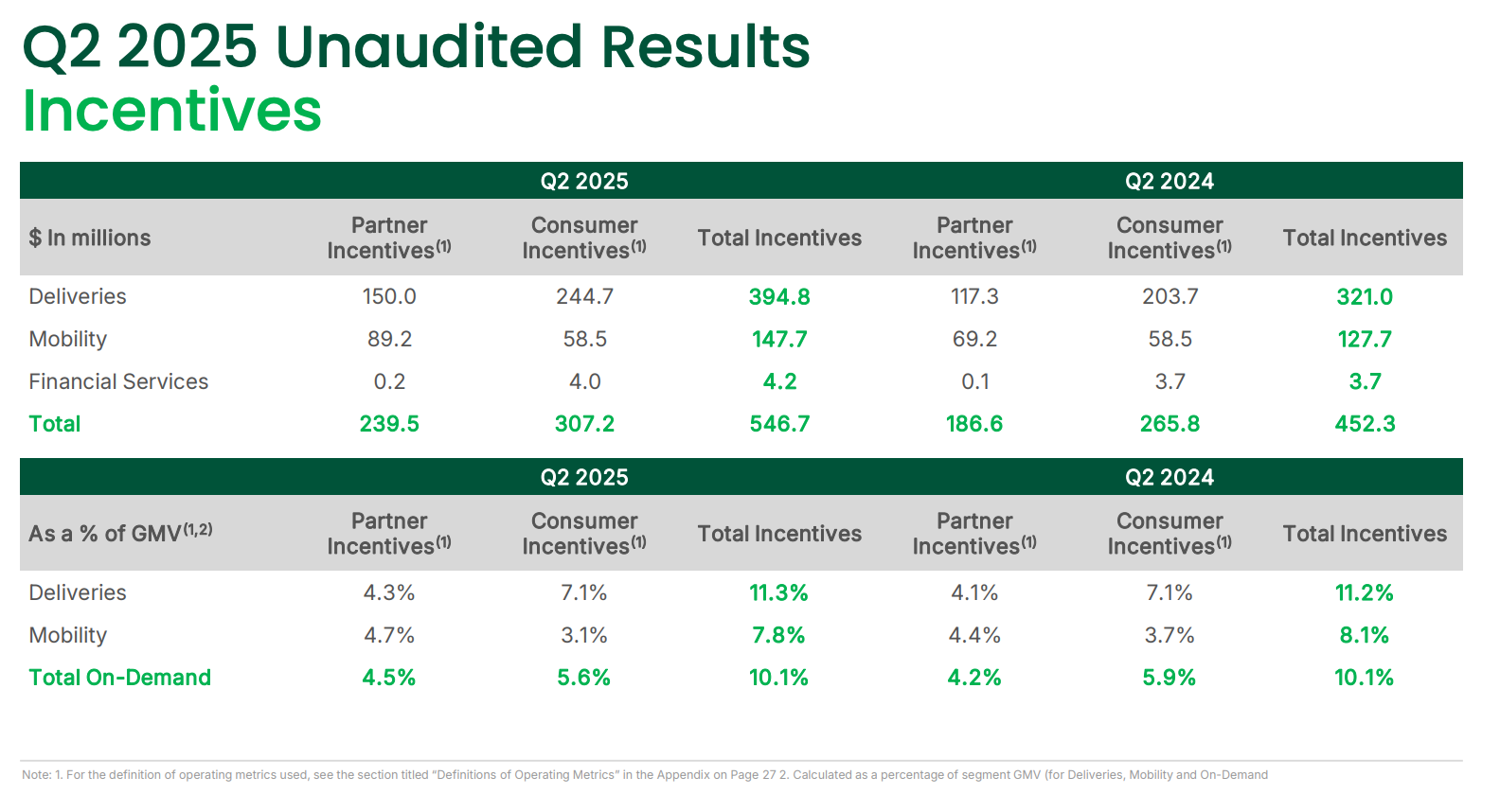

Incentives. Currently, Grab offers a large amount of incentives to accelerate growth and strengthen its flywheel for consumers and merchants. In Q2 2025, incentives reached almost 10.1% of GMV, as compared to 5.9% in Q2 2024. That’s a significant expenditure that’s artificially suppressing earnings. If Grab begins to feel comfortable taking the foot off the incentive gas pedal, this spend drops straight to the bottom line.

Three Legged Stool

One of the most simple, beautiful methods we’ve come across for framing companies is Chuck Akre’s Three Legged Stool. The three “legs” or parts of the model are:

Exceptional Business: strong moat, economics, durable profitability.

Talented Management: Highly capable and ethical leadership focusing on the long term. This usually takes the form of a founder-owner-operator, with the rare exception of a non-founder CEO.

Great Reinvesting: Earnings must be reinvested at high rates of return (greater than the benchmark) through any number of capital allocation strategies including acquisitions.

Businesses that check all the boxes of the Three Legged Stool usually demand high multiples. And they should. These business are such efficient compounders that they very quickly grow into their multiples, frequently causing a re-rating. Think of companies like Mastercard, Visa, and Moody’s who demand multiples near 40 times.

GRAB 0.00%↑ doesn’t quite yet qualify, and you can tell by its chart.

BUT, here’s the catch.

Grab is an exceptional business. It has talented management. What it doesn’t have is high returns. And how can it? It’s only just becoming GAAP profitable.

Now, what happens in 2027 when Grab produces $0.271 of earnings per share (an analyst average)? At a multiple of 40x, that implies a share price of $10.84. In two years.

By then, Grab will already have gone through another two Grab X events, rolling out what we expect to be countless number of new products and services.

Valuation

Grab’s business segments include Mobility, Deliveries, Financial Services, and Enterprise. Based on Q2 2025 results, Mobility generated $247 million in revenue (30% of total), Deliveries $356 million (43%), Financial Services $60 million (7%), and Enterprise $156 million (19%), for a quarterly total of $819 million. Annualizing and aligning with 2025 guidance of $3.33-3.40 billion total revenue, we estimate 2025 segment revenues at Mobility $988 million, Deliveries $1.42 billion, Financial Services $240 million, and Enterprise $624 million.

Projecting to 2027 with differentiated growth rates, 18% annually for Mobility, 22% for Deliveries, 40% for Financial Services, and 25% for Enterprise, yields 2027 revenues of Mobility $1.38 billion, Deliveries $2.11 billion, Financial Services $470 million, and Enterprise $975 million.

Aggregating these projections gives a 2027 total revenue estimate of $4.938 billion, reflecting 21.4% compound annual growth from the 2025 midpoint of $3.35 billion. Assuming adjusted EBITDA margins expand to 20% by 2027 (from 14% in 2025 guidance), EBITDA reaches $987 million. After deducting estimated depreciation, stock-based comp, interest/taxes, and others, we estimate net income reaching roughly $580 million. With ~4 billion outstanding shares, applying a 40x multiple lends to what we believe is a conservative present share price of $5.80.

By 2027, we think there’s a chance for growth to accelerate. If it doesn’t and remains around 20-22% top-line growth, with 30% bottom-line growth, we think a share price of $11 could leave Grab undervalued. This would be a CAGR of 37% over the next two years. We’re optimistic.

Closing Thoughts

Grab is a phenomenal business, in a region with very encouraging tailwinds. As we look 10 years out into the future, Grab is a business that could only grow stronger. As it prioritizes consumers, solving real world problems for people, Grab creates an symbiotic ecosystem where products and services compliment each other. The data collected on users and merchants creates tailored offerings, kicking off flywheels on both the consumer and merchant side of the business. As these offerings scale, the generated earnings will drop straight to the bottom line, providing significant operating leverage. Grab will be encouraged to deploy it’s $7 billion in cash through acquisitions, buybacks, or other methods of growth.

As of October 27th 2025, GRAB 0.00%↑ is a $6 stock. By 2027, we expect GRAB 0.00%↑ to reach $11 per share.

Acknowledgements

Amits Deep Dives’s Grab Thesis

Chit Chat Stocks Newsletter’s Grab Writeup

Let us know what you think in the comments, or message us in our chat.